Exploring the Benefits and Risks of Mortgage Forbearance

Is mortgage forbearance a good idea? The recent pandemic has put many homeowners in a difficult situation, struggling to make ends meet and keep up with their mortgage payments. As a result, many are turning to the option of mortgage forbearance to stay afloat during this time. But is it really a good idea?

In this article, we explore the concept of mortgage forbearance, outlining its advantages and disadvantages so you can decide if it’s right for your financial situation. We’ll look at different scenarios where mortgage forbearance may be beneficial and offer advice on how best to proceed when considering this option.

Mortgage forbearance comes with risks but offers some relief for those who need it most during these uncertain times. With the proper knowledge and understanding of all angles of this decision-making process, you can determine whether it makes sense for you. So let’s dive into the pros and cons of choosing mortgage forbearance.

What is Mortgage Forbearance?

Mortgage forbearance is when a lender temporarily allows a borrower to make reduced or suspended payments on their mortgage. This helps people who are facing financial hardship due to a job loss, illness, or other emergency. It’s important to note that mortgage forbearance is not a permanent solution and will need to be paid back in the future.

Pros And Cons Of Mortgage Forbearance

Pros:

- Mortgage forbearance can provide temporary relief from having to make mortgage payments, which can be a huge benefit for homeowners who are struggling financially.

- It can provide a reprieve from foreclosure, allowing homeowners to stay in their homes while they figure out their financial situation.

- It can give homeowners time to explore other options such as loan modifications or refinancing.

- It can provide peace of mind knowing that the mortgage payments are being temporarily suspended.

Cons:

- Mortgage forbearance can negatively impact a homeowner’s credit score, as missed payments are still reported to the credit bureaus.

- Interest will continue to accrue on the unpaid balance, adding to the overall debt.

- If the forbearance period is not extended, the homeowner may face an even larger financial burden once the payments resume.

- The homeowner must still pay the full amount due at the end of the forbearance period, which may be difficult for those who are already struggling financially.

Considering mortgage forbearance is a big decision, it’s essential to understand the pros and cons. On the one hand, this type of foreclosure prevention can allow homeowners to temporarily reduce or suspend their monthly payments without accruing additional late fees or penalties. This could be critical for those facing short-term hardship due to job loss, medical issues, military deployment, etc. On the other hand, if a homeowner qualifies for forbearance and follows through on repayment terms post-forbearance period, then they will not have any negative impact on their credit score.

On the other hand, if misused, mortgage forbearance could lead to long-term financial strain as missed payments during the period of forbearance will still need to be repaid in full – either by refinancing the loan or making lump sum payments when able. In addition, interest continues accumulating, meaning that even after resuming regular payments, far more money has been paid out than usual. Ultimately each situation must be weighed individually, and professional advice should always be sought before entering into such an agreement with your lender. Nevertheless, with careful consideration of all factors involved, mortgage forbearance may prove beneficial in certain cases where other options are not available.

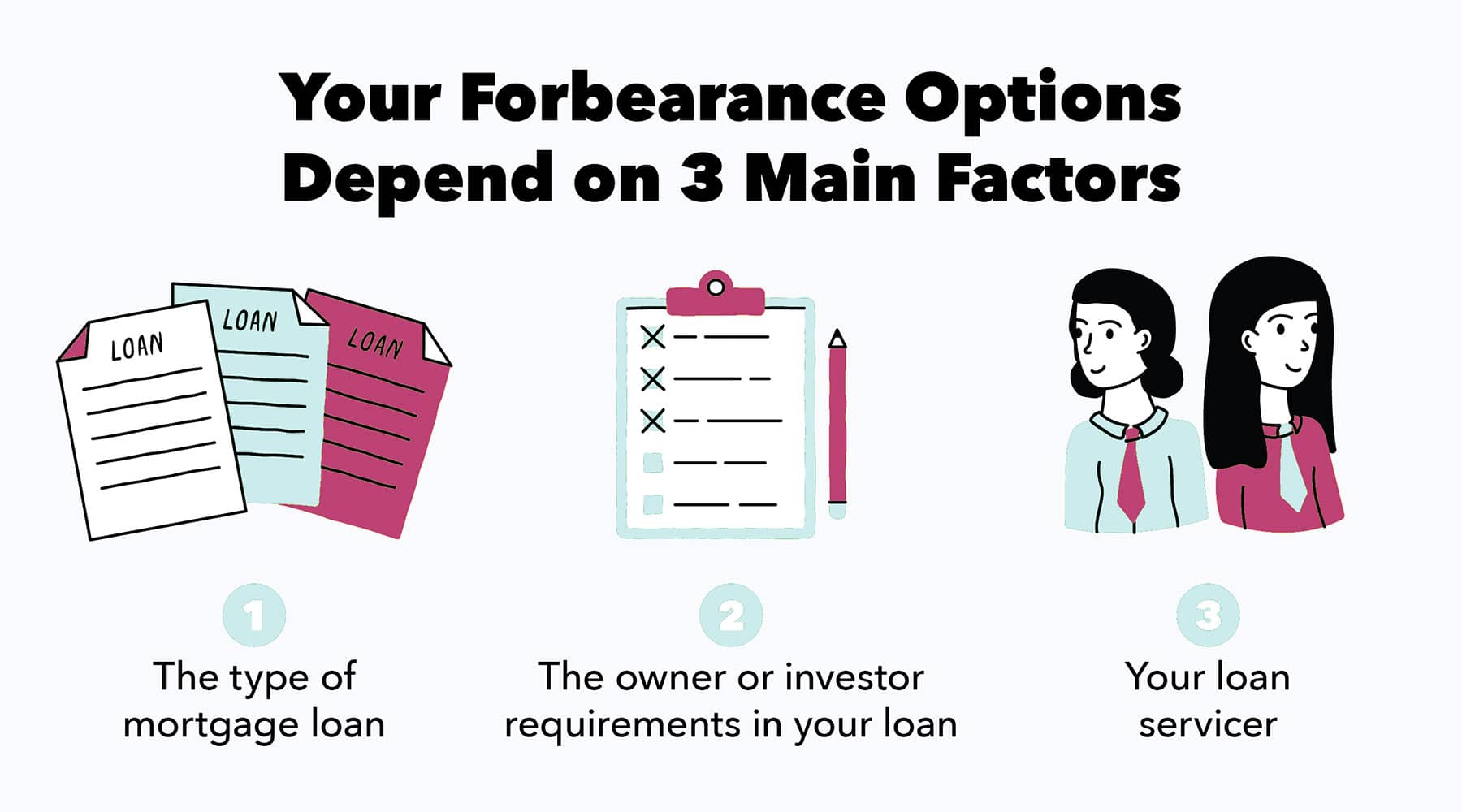

Qualifying for mortgage forbearance requires meeting specific criteria determined by lenders, which will vary depending on individual circumstances and state laws governing foreclosures. It’s essential that prospective borrowers fully understand what requirements must be met prior to applying so they know exactly what conditions they’ll have to abide by should they receive approval.

Qualifying For Mortgage Forbearance

Mortgage forbearance is a great option for borrowers struggling to make payments due to unforeseen circumstances. In order to qualify, there are several criteria that must be met:

- The borrower must prove financial hardship.

- Mortgage lenders will take into account the loan-to-value ratio of the property and other factors before approving a forbearance request.

- Borrowers should also have a history of making on-time payments prior to requesting forbearance.

- A reasonable plan demonstrating how the borrower intends to pay back missed or reduced payments may need to be provided as well.

It’s important to note that while mortgage forbearance can provide temporary relief from payment obligations, it is not an indefinite solution and requires careful consideration in determining if this type of arrangement is right for you and your situation. Moving forward, exploring alternatives to mortgage forbearance may offer an even more suitable option for some borrowers who find themselves facing difficulty with their home loans.

mint-intuit.com

Tax Implications Of Mortgage Forbearance

Consult a tax professional for the most accurate tax advice.

When deciding whether mortgage forbearance is a good idea, it’s important to consider the tax implications. The IRS generally views any amount of debt forgiven or deferred as taxable income. That means if your lender agrees to modify terms so you don’t have to pay some portion of what you owe on your mortgage loan, then you may be liable for taxes on that amount.

This only sometimes applies in some situations, though. Suppose you borrowed money from someone other than a financial institution, like a friend or family member, and they agree not to make you pay back the full amount due. In that case, this isn’t considered taxable income by the IRS. It’s also possible that your state offers tax breaks when it comes to mortgage forbearance agreements, so check with them before making any decisions about taking advantage of this option. Ultimately, understanding how taxes will factor into your decision can help determine if this type of agreement is right for you. With potential future consequences in mind, proceed with caution and research all options thoroughly before moving forward.

So, Is Mortgage Forbearance A Good Idea?

Mortgage forbearance can be a good idea for some people in certain circumstances. It can help provide temporary relief from making mortgage payments, but it does not erase the debt. Interest will continue to accrue during the forbearance period and the missed payments must be paid back at a later date. This can be a good option for those who need relief in the short term, but it’s important to consider all options before making a decision. In some cases, it may be beneficial to explore alternatives such as loan modification or government programs like HAMP that are designed to help borrowers stay in their homes and avoid foreclosure.

For example, The Storck Team has worked with clients who were struggling financially due to job loss caused by COVID-19. After considering all options, we decided mortgage forbearance was the best choice since it allowed them to suspend payments without any major repercussions. This gave enough time to secure new employment while avoiding defaulting on the loan, which would have had serious consequences down the road.

In conclusion, mortgage forbearance can provide much-needed relief during times of financial hardship but should only be taken after careful consideration of your own unique circumstances. As professional real estate agent, I highly recommend consulting a qualified professional before making any decisions regarding your home loan so you don’t end up in more debt than when you started. Contact The Storck Team to explore your options.

{kind=link}

{kind=link}

{kind=link}

{kind=link}